Firms and LLPs now deduct TDS when they pay a partner. This free 194T TDS calculator works out the tax in seconds: enter the salary, interest and commission you pay a partner in the year, and it shows whether the Rs 20,000 limit is crossed and the 10% TDS to deduct for Tax Year 2026-27.

Share of profit and drawings of capital are not counted here, they are outside 194T. TDS is deducted at the earlier of credit to the partner account or actual payment. This tool is for guidance for Tax Year 2026-27.

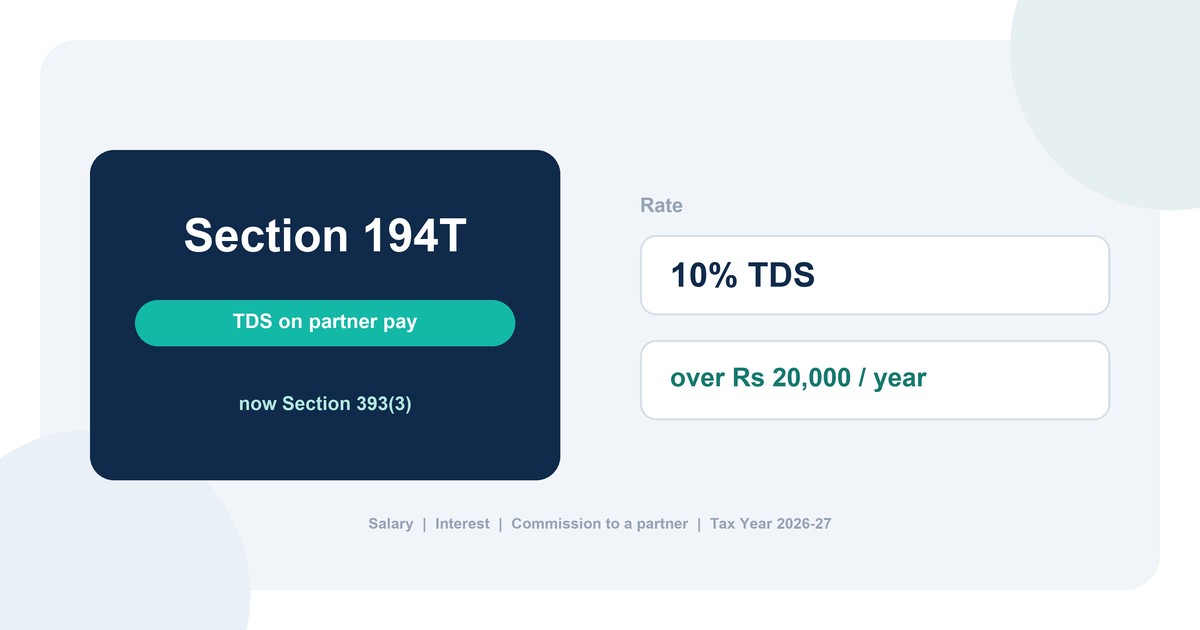

Quick answer: deduct 10% TDS on salary, interest, commission and bonus paid to a partner, once the yearly total crosses Rs 20,000. The 10% then applies to the whole amount, not just the part above Rs 20,000.

What Section 194T is, in simple words

Until recently, when a firm paid its own partner a salary or interest on capital, there was no TDS on it. Section 194T changed that from 1 April 2025. Now a firm or LLP holds back a little tax on those partner payments and sends it to the government, exactly like it already does for a contractor or a professional. From 1 April 2026 the rule moves into the new law as part of Section 393(3), but the numbers are the same.

How the 194T TDS calculator works

The 194T TDS calculator adds up every kind of payment you make to one partner in the year: salary or remuneration, interest on capital or loan, and any commission or bonus. If the total is Rs 20,000 or less, there is no TDS. If it is more, it applies 10% to the entire total. If the partner has not given a PAN, the rate becomes 20%.

What counts and what does not

- Counted: salary, remuneration, bonus, commission and interest on capital or loan paid to the partner.

- Not counted: the partner share of profit and any drawing or repayment of capital. These sit outside Section 194T.

A quick example

Suppose a firm pays a partner Rs 5,00,000 as remuneration and Rs 1,00,000 as interest on capital in the year. The total is Rs 6,00,000, which is above Rs 20,000, so TDS applies. At 10% the firm deducts Rs 60,000 and pays the partner Rs 5,40,000. The partner later adjusts that Rs 60,000 against their own tax.

Where 194T sits in the new law

The old 194-series TDS sections have been folded into a single Section 393 of the Income-tax Act 2025. Partner payments sit in the special sub-section 393(3), at Table serial number 7, with e-Pay Tax payment code 1067. You can look up any old TDS section in our Section 393 mapping tool.

Need partner TDS set up for your firm?

Our team runs TDS compliance for businesses end to end: monthly challan payments with the correct codes, quarterly returns, Form 16 and the new Form 130 certificates, and notice responses. Tell us about your setup and we will reply with a plan and a quote within one working day.

Frequently asked questions

What is Section 194T?

Section 194T makes a firm or LLP deduct TDS on money it pays a partner: salary, remuneration, commission, bonus and interest on capital or loan. It began on 1 April 2025. Under the new Income-tax Act 2025 the same rule sits in Section 393(3), Table serial number 7, with e-Pay Tax code 1067, from 1 April 2026.

What is the 194T TDS rate and threshold?

The rate is 10%. There is no TDS if the total of all such payments to a partner is Rs 20,000 or less in the financial year. Once the total crosses Rs 20,000, TDS at 10% applies to the whole amount, not only the part above Rs 20,000.

Is TDS deducted on the whole amount or only the excess over Rs 20,000?

On the whole amount. The Rs 20,000 is only a trigger. If a partner is paid Rs 25,000 for the year, TDS is 10% of Rs 25,000, which is Rs 2,500, not 10% of the Rs 5,000 above the limit.

Does 194T apply to a partner share of profit?

No. A partner share of profit is not covered, and neither is a withdrawal of capital. Section 194T applies only to salary, remuneration, commission, bonus and interest paid to the partner.

What if the partner has no PAN?

If the partner has not given a valid PAN, TDS is deducted at the higher rate of 20% under Section 397, the new version of the old Section 206AA. Uncheck the PAN box in the calculator to see this.

When must the firm deduct and deposit the 194T TDS?

The firm deducts at the earlier of crediting the amount to the partner account (including the capital account) or paying it. The tax is then deposited by the 7th of the next month, following the usual TDS calendar.

Official source: Confirm the current rule and rate on the new Act pages at incometax.gov.in.

Related: Section 393 TDS mapping tool · TDS rate calculator · TDS due dates FY 2026-27