Everyone makes tax mistakes. A bank FD you forgot, freelance income you did not think counted, or a year you simply never filed. ITR-U, the updated return, is the government official second chance: you can fix an old return, or file a missed one, up to 48 months after the year ends. This guide explains it the way a friend would: what it is, exactly what it costs with full calculations, which years you can still fix today, and every click of the filing process.

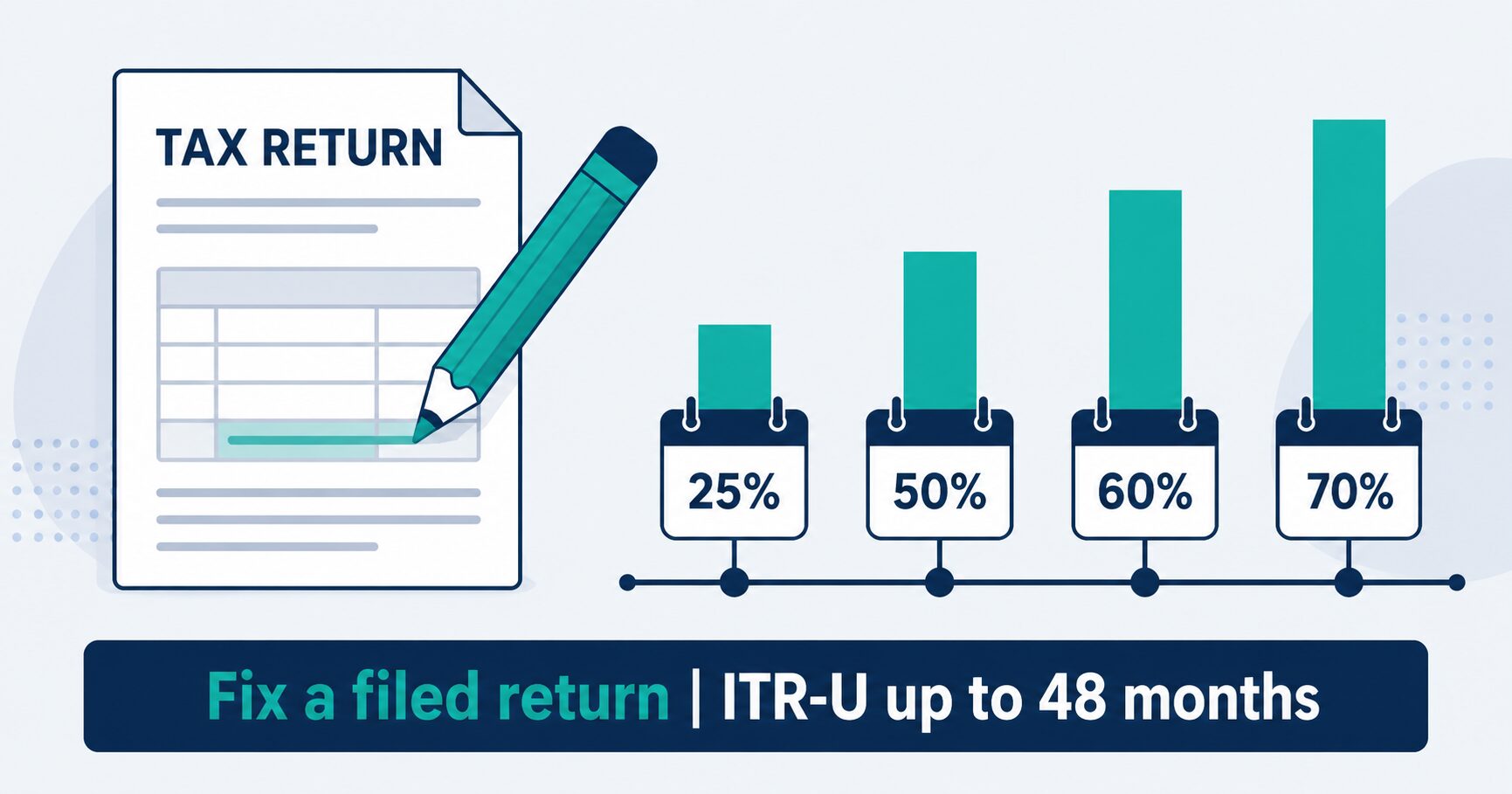

Quick answer: ITR-U (Section 139(8A)) lets you declare missed income for the last four assessment years by paying the tax, the interest, and an extra fee called additional tax: 25% in year one, then 50%, 60% and 70% of the tax plus interest. You cannot use it to claim a refund. File early: the same mistake gets more expensive every 12 months.

What is ITR-U, in truly simple words

Think of your tax return as an exam answer sheet. Normally, once you hand it in, it is done. A revised return is like the teacher letting you swap answer sheets before marking begins; that door closes on 31 March of the assessment year. ITR-U is different: it is the school letting you reopen your answer sheet years later, but charging a growing fee for the privilege. The government wins because it collects tax it may never have found; you win because you sleep at night and avoid a much scarier penalty later.

Three words you will see everywhere, defined once:

- Assessment year (AY): the year in which a return for the previous financial year is filed and checked. Income you earned in FY 2024-25 is filed in AY 2025-26. The 48-month ITR-U clock runs from the END of the assessment year.

- Additional tax: the extra fee for using ITR-U. It is a percentage of the tax plus interest you owe on the missed income, not a percentage of the income itself.

- CPC: the Centralised Processing Centre in Bengaluru, the automated system that checks every return. Its computers compare your return with the AIS, so unreported interest and trades are exactly how people get caught.

Who can file ITR-U, and who cannot

You missed income in a filed return. You never filed at all. You picked the wrong income head. You need to pay more tax for any reason. From 1 March 2026 you can even file one that reduces a loss you had claimed, provided the original loss return was filed on time.

The change would lower your tax or create or increase a refund. A search or survey is running against you. You already filed an ITR-U for that year (one shot per year). The result is a nil change with no extra tax to pay.

What ITR-U actually costs, with the full maths

The bill has four parts: the tax on the missed income, interest under Sections 234A, 234B and 234C, the late fee under Section 234F if you never filed the original return, and then the additional tax on top. The additional tax depends only on how late you are:

| When you file (from end of the AY) | Additional tax |

|---|---|

| Within 12 months | 25% of tax + interest |

| 12 to 24 months | 50% of tax + interest |

| 24 to 36 months | 60% of tax + interest |

| 36 to 48 months | 70% of tax + interest |

Example 1: Ravi and the forgotten FD interest

Ravi is a salaried employee. He filed his AY 2025-26 return on time, but forgot Rs 40,000 of FD interest that his bank reported to the AIS. He files an ITR-U in August 2026, which is within 12 months of 31 March 2026, so the 25% band applies. His slab rate is 20%:

- Tax on Rs 40,000 at 20% = Rs 8,000, plus 4% cess = Rs 8,320

- Interest under 234B and 234C for the delay, roughly Rs 1,180

- Additional tax = 25% of (8,320 + 1,180) = Rs 2,375

- Total payable: about Rs 11,875. No 234F fee, because his original return was filed on time.

If Ravi waits until May 2027 for the same fix, the band becomes 50% and the additional tax alone doubles to about Rs 4,750, plus extra months of interest. Same mistake, bigger bill.

Example 2: Meena, who never filed at all

Meena earned Rs 8,00,000 as a freelancer in FY 2023-24 (AY 2024-25) and never filed a return. Her tax works out to about Rs 23,400. Filing an ITR-U in July 2026 lands in the 50% band (12 to 24 months from 31 March 2025):

- Tax + cess = Rs 23,400

- Interest under 234A, 234B and 234C, roughly Rs 5,100

- Late fee under 234F (income above Rs 5 lakh) = Rs 5,000

- Additional tax = 50% of (23,400 + 5,100) = Rs 14,250

- Total payable: about Rs 47,750 to become fully compliant for that year.

Why pay it at all? Because the alternative is worse. If the department finds the income first, the under-reporting penalty under Section 270A is 50% of the tax, and 200% if it counts as misreporting, on top of everything above, plus possible prosecution for larger amounts. ITR-U is the discounted exit.

Which years can you still fix, as of July 2026

| Assessment year (income year) | Band if you file NOW | Band rises next on | Final ITR-U deadline |

|---|---|---|---|

| AY 2025-26 (FY 2024-25) | 25% | 1 April 2027 (to 50%) | 31 March 2030 |

| AY 2024-25 (FY 2023-24) | 50% | 1 April 2027 (to 60%) | 31 March 2029 |

| AY 2023-24 (FY 2022-23) | 60% | 1 April 2027 (to 70%) | 31 March 2028 |

| AY 2022-23 (FY 2021-22) | 70% | Already in the last band | 31 March 2027 |

Closing forever: AY 2022-23 shuts permanently on 31 March 2027. If FY 2021-22 has a skeleton, this is the last exit. And note the current return, AY 2026-27, cannot use ITR-U yet; fix it free with a revised return until 31 March 2027 instead.

What the Finance Act 2026 changed, from 1 March 2026

- Loss returns can now be updated. Earlier, if your original return declared a loss, ITR-U was blocked. Now you can file one that reduces the loss, as long as the original loss return was filed by the due date.

- ITR-U after a reassessment notice. Earlier, a Section 148 notice slammed the ITR-U door shut. Now you can file within the time given in the notice, paying an extra 10 percentage points (so 35%, 60%, 70% or 80%). In exchange, the new Section 270A(11A) shield means the income you disclose this way cannot be used to charge the under-reporting penalty. Filing does not automatically close the reassessment, so take advice in notice cases.

How to file ITR-U, click by click

- Work out the bill first. Compute the missed income, the tax and cess, the interest, the 234F fee if the original was never filed, and the additional tax band from the table above. The ITR-U form (Part B-ATI) asks for these figures explicitly.

- Pay the tax before filing. Log in at incometax.gov.in, go to e-File, then e-Pay Tax, choose the correct assessment year, and pay under the self-assessment head. Keep the challan number; the form asks for it. The payment screens work exactly like our e-Pay Tax walkthrough.

- Start the return. Go to e-File, then Income Tax Returns, then File Income Tax Return. Pick the assessment year you are fixing, then choose the filing type 139(8A), Updated Return.

- Fill your normal ITR plus the ITR-U part. You file the same ITR form that applies to you (ITR-1 to ITR-4 for most people; use our form picker if unsure) with the corrected figures, and the ITR-U wrapper asks two extra things: the reason (a dropdown: income not reported correctly, wrong head, return not filed earlier, and so on) and the Part B-ATI tax computation with your challan details.

- Verify within 30 days. E-verify with Aadhaar OTP or net banking. An unverified ITR-U is treated as never filed.

The mistakes that get ITR-U filings rejected

- Paying after filing instead of before. The additional tax must be paid and the challan quoted inside the form, or the return is invalid.

- Using it to claim a refund. The utility will simply block a return where the tax payable falls. That correction needed a revised return, whose window has closed.

- Wrong band arithmetic. The 25% to 70% applies to tax PLUS interest, not tax alone, and not the income.

- Forgetting the second year. If you missed FD interest in one year, you probably missed it in the next too. Check the AIS for each year before filing.

- Missing the one-shot rule. Only one ITR-U per assessment year, ever. Get it complete the first time.

How people discover they need ITR-U

Almost always from the AIS, the Annual Information Statement, which lists every interest credit, dividend, share sale and property deal reported against your PAN. Pull it for the past years, compare it with what you filed, and you will know in ten minutes whether you have a gap. Our AIS vs 26AS vs TIS guide shows exactly how to read it, and our Section 234 interest calculator estimates the interest part of your bill.

Need help fixing an old return?

Filing an ITR-U wrong wastes the one chance you get per year. Our team computes the exact tax, interest and additional tax, prepares the updated return with the correct reason codes, and files it. Tell us which year and what was missed, and we will reply with a quote within one working day.

Frequently asked questions

What is ITR-U in simple words?

ITR-U is the updated return. It is a second chance to correct an income tax return you already filed, or to file one you missed completely, up to 48 months after the end of the assessment year. The catch is a fee called additional tax: the longer you wait, the more you pay, from 25% up to 70% of the tax and interest involved.

What is the last date to file ITR-U right now?

Each year has its own deadline. As of July 2026 you can still file ITR-U for AY 2022-23 (until 31 March 2027 at 70%), AY 2023-24 (60% until 31 March 2027), AY 2024-25 (50% until 31 March 2027) and AY 2025-26 (25% until 31 March 2027). The earlier you file, the cheaper the band.

Can I claim a refund by filing ITR-U?

No. ITR-U exists only to declare more income and pay more tax. You cannot use it to reduce your tax, claim a new refund or increase an old one. If you need to lower your income or claim a missed deduction, that had to be done through a revised return before 31 March of the assessment year.

Can I file ITR-U if I never filed the original return?

Yes. ITR-U works even if you never filed for that year. You will also pay the Section 234F late fee (Rs 5,000 if your total income is above Rs 5 lakh, otherwise Rs 1,000) on top of the tax, interest and additional tax.

What happens if I got a Section 148 reassessment notice?

From 1 March 2026, under the Finance Act 2026, you can file ITR-U even after a Section 148 notice, within the time given in the notice. It costs an extra 10 percentage points of additional tax (so 35% to 80% instead of 25% to 70%), but the income you disclose this way cannot then be used to levy the Section 270A penalty, which can otherwise be 50% to 200% of the tax.

Do I need a CA to file ITR-U?

Not necessarily. If the correction is simple, like missed bank interest, the portal walks you through it and this guide covers each step. If the missed income is large, spans several years, or a notice is already involved, a professional is worth the fee because the additional-tax maths and the reason codes must be exactly right.

Official source: The updated-return provisions and the current utility are on incometax.gov.in.

Related: Which ITR form to file · AIS vs 26AS vs TIS · Section 234 interest calculator · How to pay tax online