AI in finance and accounting is moving fast, and this guide is a plain English look at what it can actually do, where the real potential is, and how to start using it well. It is written for accountants and finance teams, not for engineers, so there is no jargon and nothing to install to follow along. By the end you will know what AI in finance and accounting can take off your plate today, which tasks suit which AI model, how to bring it in safely, and how to get better at it over time. This guide is deliberately vendor neutral, so it is about the technology and how to use it well, not about any one product.

What AI can actually do in accounting and finance

Here is what AI in finance and accounting can genuinely do today.

There is a lot of noise about AI right now, and most of it does not explain what the technology genuinely does once it is pointed at a set of books. So let us be plain. Modern AI is very good at reading messy real world documents, recognising patterns across thousands of transactions, and turning structured numbers into readable language. It is not a calculator and it is not magic. Think of it as a fast, tireless junior who has seen millions of invoices and ledgers, who never gets bored of repetitive work, and who always shows you the source so you can check. The capabilities below are already in everyday use across finance and accounting teams. Read each one as a building block. On their own they are useful. Stitched together, they change how a month looks.

Reading and extracting from documents

This is the foundation that the rest of AI in finance and accounting builds on.

It is the bedrock the rest of this builds on. Point AI at a purchase invoice, a vendor bill, a bank statement, a salary slip, an expense receipt or a contract, and it pulls out the fields that matter: vendor name, GSTIN, invoice number, date, taxable value, the current tax slab applied (0, 5, 18 or 40, plus any special rate or cess), line items, and totals. It does this whether the document is a clean PDF, a blurry photo taken on a phone, a scanned page, or an email body with the figures buried in a sentence. Crucially, it does not need a fixed template for each vendor the way old rule based scanners did. It reads the way a person reads, by understanding the layout and the meaning, so a new supplier format does not break it. This single capability removes most manual data entry, which is where a great deal of an accountant’s day quietly disappears.

Classifying and coding transactions to the right ledger

Coding is one of the biggest everyday time savers in AI in finance and accounting.

Once a transaction is read, it has to be put somewhere. AI can look at a description, a vendor, an amount and the history of how similar items were treated, and suggest the correct ledger, cost centre and tax treatment. A payment to a courier service gets coded to freight, a software renewal to subscriptions, a hotel bill split between travel and the right input tax, and so on. Because it learns from how your own team has coded things in the past, it adapts to your chart of accounts rather than forcing a generic one on you. The accountant moves from typing every line to reviewing and approving, correcting the few it gets wrong, and the system gets better each time you correct it.

Reconciling bank, GST and intercompany accounts

Matching across imperfect data is where AI in finance and accounting is especially strong.

Reconciliation is matching: this entry in the books against that line on the statement. AI is strong here because matching across imperfect data is exactly what it is built for. For bank reconciliation it pairs book entries with bank lines even when amounts are split, dates differ by a day or two, or descriptions are written differently on each side. For GST it compares your purchase register against the GSTR-2B downloaded from the portal, flags invoices that are in your books but missing from 2B, those in 2B but not in your books, and mismatches in value or tax, so you can chase the right vendor before you claim input credit. For intercompany it lines up what one entity recorded as a payable against what the other recorded as a receivable and surfaces the differences. The work that used to mean scrolling two spreadsheets side by side becomes a short list of genuine exceptions to investigate.

Drafting reports and plain language MIS commentary

Turning numbers into words is a natural fit for AI in finance and accounting.

Numbers alone do not tell management what happened. AI can take a finished trial balance or a set of monthly figures and write the narrative around them: revenue rose against last month, this expense head jumped and here is the likely reason, margins moved this way, receivables are ageing. It produces the kind of MIS commentary a finance manager would otherwise spend an evening writing, in clear sentences a non finance reader can follow, and it can redo it in seconds when a number changes. You still own the judgement and the final wording, but you start from a solid draft instead of a blank page.

Forecasting and scenario building

Looking ahead is one of the most valuable uses of AI in finance and accounting.

Because AI can read history quickly, it can project it forward. Feed it past sales, collections, payments and expenses and it can build a cash flow forecast, estimate next quarter’s revenue, or model what happens to runway if collections slow by a few weeks. The real value is in scenarios. You can ask what the year looks like if a large customer pays late, if input costs rise, or if you add a new line of business, and get a comparison of outcomes side by side. This turns planning from an annual ritual into something you can rerun whenever a real question comes up.

Spotting anomalies and possible fraud

Catching the odd one out is a quiet but important role for AI in finance and accounting.

An attentive AI watches every transaction, not a sample. It learns what normal looks like for your business and then flags what does not fit: a duplicate payment to the same vendor, an invoice value far outside the usual range, a round number that looks manufactured, a supplier whose bank details suddenly changed, expenses claimed on a weekend or a holiday, or a sequence of entries just under an approval threshold. None of these are proof of wrongdoing, and the system does not accuse anyone. It simply raises a hand and says this one is unusual, please look, which is exactly the early warning a busy team rarely has time to generate by hand.

Supporting audit and compliance

Audit support shows AI in finance and accounting at its most practical.

AI helps both the people being audited and the people auditing. It can assemble the supporting documents for a sample, check that every entry has a backup, confirm that tax has been applied at the correct slab, and test a whole population of transactions against a rule rather than just a sample of them. It can read a long agreement and pull out the clauses that affect revenue recognition, payment terms or penalties. For statutory and GST compliance it can cross check that what was filed agrees with what is in the books and flag gaps early. The auditor still signs off and applies professional judgement. The AI removes the hours of fetching, ticking and cross referencing that come before that judgement.

Answering plain language questions about the books

This makes AI in finance and accounting useful to people who are not specialists too.

Perhaps the most natural capability of all is conversation. Instead of building a report or writing a query, you can simply ask: which customers owe us money for more than ninety days, how much did we spend on travel last quarter, what is our input tax credit position this month, show me every payment above a certain amount to a particular vendor. The AI reads your data and answers in plain English, often with the underlying figures so you can verify. This puts the books within reach of people who are not trained to navigate accounting software, such as a founder, an operations head or a partner who just wants a straight answer.

The Real potential for your team

Put together, this is the real promise of AI in finance and accounting.

Put these capabilities together and the gains are concrete rather than vague. Here is what teams in accounting and finance can realistically expect.

- Hours given back from repetitive work. Data entry, document sorting, line by line coding and manual matching are the tasks that eat the most time and add the least judgement. Handing the first pass to AI frees up a meaningful share of every week, and that time compounds across a whole team and across every month of the year.

- Fewer errors, and the same standard every time. A tired person at the end of a long day transposes a figure or codes a bill to the wrong head. AI applies the same logic to the first transaction and the ten thousandth, and because it flags its own uncertain cases for a human to check, the mistakes that do slip through are caught earlier rather than at year end.

- Faster month end closes. When reading, coding and reconciliation happen continuously through the month instead of in a frantic rush at the start of the next one, the close shrinks from a long week of late nights to a short, calm review. Books that were ready on the fifteenth can be ready on the third.

- Real time visibility. Because transactions are processed as they arrive, management does not have to wait for a closed month to know where things stand. Cash position, receivables, payables and spend are current, so decisions are made on today’s picture rather than last month’s.

- The ability to scale without adding headcount. When the volume of invoices doubles, or a second and third entity come on board, the workload normally means hiring. With AI carrying the repetitive load, the same team can handle far more clients, entities and transactions, which matters enormously for a practice that wants to grow or a finance function under pressure to do more with the same budget.

- Skilled people freed for judgement and advisory work. This is the real prize. Qualified accountants did not train for years to type invoice numbers. When the routine is handled, their time shifts to the work only a human can do: interpreting what the numbers mean, advising on tax and structure, improving controls, sitting with clients, and guiding decisions. The role moves up the value chain, from recording the past to shaping the future, and that is both more useful to the business and far more satisfying to do.

None of this asks you to hand over control or to trust a black box. The pattern that works is simple and steady: AI does the heavy, repetitive first pass and always shows its working, and a skilled person reviews, corrects and approves. That is the honest promise of AI in finance and accounting today. Not a replacement for your expertise, but a powerful assistant that clears away the drudgery so your expertise can finally be spent where it counts.

Where AI helps, function by function

AI in finance and accounting is most useful where the work is high volume and rule based. The table below is a quick summary of where it helps, what it does, and what you get out of it.

| Finance function | How AI helps | What you get |

|---|---|---|

| Accounts payable | Reads each invoice, pulls out the vendor, amounts, GST and dates, suggests the ledger and routes it for approval. | Bills posted in minutes, not hours, with fewer keying errors. |

| Bank reconciliation | Matches bank statement lines to ledger entries and flags what does not match. | A faster, cleaner monthly close. |

| GST and tax | Matches purchase records against the GSTR-2B return and highlights gaps. | Cleaner input tax credit matching and earlier sight of mismatches. |

| MIS and reporting | Builds dashboards and writes plain language commentary on trends and variances. | Decisions backed by numbers, sooner. |

| Expenses and fraud | Spots duplicate bills, odd amounts and policy breaches before payment. | Less leakage and stronger controls. |

| Collections | Predicts which customers will pay late and drafts polite reminders. | Better cash flow and less chasing. |

| Audit and compliance | Samples transactions, runs checks and documents the trail. | Less manual review at audit time. |

Which AI model for which task

Different models are good at different jobs, and a strong approach to AI in finance and accounting picks the right one for each task rather than forcing one model to do everything. Here is how the main models compare.

The table below is a quick guide for common tasks.

| Finance task | Best fit AI | Why |

|---|---|---|

| Messy or multi page invoices | Claude |

Handles tricky layouts and reasons through exceptions. |

| Everyday invoice data extraction | ChatGPT |

Balanced speed, accuracy and cost for routine bills. |

| Scanned or photographed bills | Gemini |

Best on images and mixed or low quality scans. |

| High volume coding and matching | DeepSeek |

Low cost at large scale for repetitive work. |

| MIS and variance commentary | Claude or ChatGPT |

Clear, well written explanations of the numbers. |

| Bank and ledger matching | ChatGPT or DeepSeek |

Fast pattern matching across many lines. |

AI is a partner, not a competitor

Used well, AI in finance and accounting makes you stronger, not redundant.

Let us clear up the worry that sits quietly behind a lot of conversations about this technology. AI is not yet ready to run finance and accounting on its own. It does not understand your business the way you do. It does not know which vendor always sends a corrected invoice a week later, why a particular ledger was opened, or what your client actually meant in that one rushed phone call. It cannot sign off on a return, sit across the table during an assessment, or carry the responsibility when something goes wrong. So the right way to see it is simple. AI is a capable assistant that you work with, not a rival to fear and not a replacement for you.

Think of it the way a senior would think of a sharp new article. The article is fast, tireless and happy to do the repetitive work, but you would never hand over the final judgement. You check the output, you ask the questions, you catch the thing that looks off. That is exactly the relationship to have with AI in finance and accounting. It does the first pass at speed, and you bring the experience, the context and the professional eye that decides whether the work is actually right.

This matters because the parts of your job that are hardest to replace are also the most valuable. The judgement stays with you. Deciding how to treat an unusual transaction, reading whether a number feels reasonable for this client in this year, weighing a position under GST 2.0 where the standard slabs are 0, 5, 18 and 40 and special rates or cess may also apply. A tool can suggest, but it cannot be accountable. The relationships stay with you. The trust a client places in you, the calls where you explain bad news gently, the years of knowing how a family business really runs. And the final say stays with you. Nothing leaves your desk until you have looked at it and decided it is correct. AI hands you a draft. You remain the professional who signs it.

Seen this way, the technology stops being a threat and becomes leverage. It does not shrink your role. It gives you more hours to spend on the work that genuinely needs a qualified human, which is precisely the work clients are willing to pay for.

Let it take the boring, fiddly work

This is where AI in finance and accounting gives you the fastest win.

Here is the honest truth about a normal week. A surprising amount of your time goes not into thinking, but into fiddling. Nudging things into place, cleaning up messes, making files look presentable. None of it needs your training, yet all of it eats real time and leaves you tired before the actual work begins. This is exactly the kind of low value, repetitive work that AI can do in minutes. A few everyday examples:

- Aligning text and tidying the layout of a report so headings, spacing and sections line up neatly instead of you dragging things around by hand.

- Matching fonts and formatting across a document so the whole thing looks consistent, even when it was stitched together from three different sources.

- Fixing table or button borders and spacing that are uneven, so a schedule or a working sheet reads cleanly.

- Reformatting a messy bank statement or a downloaded export into clean, usable columns, instead of you copying and pasting cell by cell.

- Cleaning up duplicated or inconsistent data, like the same party name spelt four different ways, or amounts sitting in the wrong format.

- Drafting a first version of an email or a working note that you can then quickly read, correct and send in your own voice.

- Renaming and sorting files into a sensible order so you can actually find the right version later.

- Summarising a long document, such as an agreement or a circular, into a short plain summary you can scan in a minute before deciding what to do.

Notice what every one of these has in common. They are routine, they are repetitive, and none of them is why you trained for years. When you hand this kind of work to AI, you are not giving away anything important. You are clearing it off your plate so you can spend that time where it counts, on analysis, on advice, on the careful checking and the client conversations that only a professional can do. That is the real promise of AI in finance and accounting. Not a machine that replaces you, but a quiet assistant that takes the dull, fiddly tasks and hands you back your time.

Where AI falls short, and what to double check

Knowing the limits is a core part of using AI in finance and accounting well.

AI in finance and accounting can save real time, but it is a confident assistant, not a qualified reviewer. It has no stake in your books being right, and it does not feel the weight of a wrong filing the way you do. Before you lean on it, you need a clear, honest picture of where it is weak. The points below are not reasons to avoid AI. They are the exact spots where a human accountant has to stay firmly in charge.

It can hallucinate

Hallucination is the risk to watch most closely with AI in finance and accounting.

This is the single biggest risk. A hallucination is when the AI simply invents something that looks completely real but is not. It can produce a number, a vendor name, a GSTIN, an invoice reference, a section of law or a deadline that does not exist anywhere in your documents, and it will present all of it in clean, professional language. Because the made up detail sits next to genuine detail, it is very easy to miss. The AI is not lying on purpose. It is filling a gap with the most plausible looking text, and plausible is not the same as true. Treat every specific fact it gives you as unverified until you have seen it on the source document yourself.

It does not truly understand your business

The AI does not know your client, your industry, your intent or the story behind a transaction the way a person who has worked the account for years does. It does not know that a particular vendor is actually a related party, that one expense is really a personal cost routed through the firm, or that a round sum payment is a recurring arrangement you agreed months ago. It reads patterns in text. It does not hold the lived context that lets a good accountant say “that does not look right for this client.” You bring the understanding. The AI only brings the words.

It can be confidently wrong

This is why AI in finance and accounting always needs a human check.

A wrong answer from AI does not come with a warning label. It arrives in the same calm, assured, well structured tone as a correct one. There is no shake in its voice, no hedging, no “I am not sure about this part.” That steady confidence is dangerous, because it invites you to trust the output and move on. The fluency of the writing is not evidence that the content is right. Never let a smooth, certain tone stand in for verification.

It is weak on judgement, materiality and unusual situations

AI is strongest on routine, high volume, well defined tasks. It is weakest exactly where accounting needs real professional judgement. Deciding whether an item is material, how to treat a genuinely new or one off transaction, how to read an ambiguous contract clause, or how aggressive a tax position should be, these call for experience, common sense and a sense of consequence that the AI does not have. When the situation is unusual, novel or finely balanced, the AI is often least reliable and most likely to give you a confident but shallow answer.

Its knowledge of the latest rules can be out of date

Tax law, rates, slabs, thresholds and due dates change often, and an AI model is trained up to a certain point in time. It may not know the most recent notification, circular or rate change, and it can quietly answer using older rules as if they still apply. With GST, for example, an AI may not reflect the current standard slabs of 0, 5, 18 and 40, or the special rates and cess that can also apply, and it will rarely tell you that its knowledge might be stale. For anything tied to current rates, deadlines or compliance, always confirm against the official, up to date source.

It can make plain arithmetic and rounding slips

It is easy to assume a computer always adds correctly, but a language based AI is not a calculator. It can total a column wrong, drop a line, mishandle a percentage, or round inconsistently so the parts no longer tie to the whole. The mistake is often small and easy to overlook precisely because the rest of the answer looks careful. Re-add anything that matters yourself, or run it through a proper calculation tool.

It can carry bias from its data

The AI learns from large amounts of past text, and it can absorb and repeat the patterns and assumptions baked into that data. In a finance context this can show up as defaulting to one common treatment over a better suited one, leaning toward the most frequent answer rather than the correct one for your case, or quietly favouring assumptions that do not fit your client. It reflects what is common in its training, not necessarily what is right for the situation in front of you.

It cannot be accountable

This is the point that ties all the others together. The AI cannot sign a return, cannot stand behind a filing and cannot answer to a client, an auditor or a tax authority. The responsibility for every number and every decision stays with you and your firm, whether or not AI was used to produce it. The AI is a tool that helps you work, never a party that shares the blame. If the output is wrong and it goes out under your name, it is your mistake, not the machine’s.

What to double check, every time

Make this checklist a habit whenever you use AI in finance and accounting.

None of the above means you should not use AI in finance and accounting. It means you should use it the way you would use a fast but junior assistant: helpful for a first pass, never trusted without review. Run this checklist on every output before you rely on it.

- Check every amount and total against the source document. Match each figure the AI gives back to the actual invoice, statement or voucher. If it is not on the source, do not accept it.

- Re-add the totals yourself. Do not assume the maths is right. Re-total columns and subtotals by hand or in a calculator, and confirm the parts tie to the whole.

- Confirm the GST rate and tax treatment. Verify the rate, the place of supply, reverse charge where it applies and the input credit position against the current rules, not the AI’s memory.

- Confirm the ledger and the period. Make sure each entry is going to the correct ledger or head of account, and that it falls in the right accounting period.

- Watch for any vendor, GSTIN, invoice number or figure the AI may have invented. Treat every specific identifier as a possible hallucination until you have matched it to a real document.

- Be extra careful on anything material. The larger the amount or the bigger the consequence of an error, the more slowly and thoroughly you check it. Reserve your sharpest review for what matters most.

- Never accept a confident answer without verifying it. A calm, assured tone is not proof. Confidence from the AI is not a substitute for your own check.

- Always keep the source document open beside the AI output. Review the two side by side so you can verify line by line, rather than trusting the AI’s summary on its own.

Used this way, AI in finance and accounting becomes a genuine help: it does the heavy lifting on the first draft, and you stay the qualified professional who checks, corrects and signs off. The tool speeds you up. The judgement, and the responsibility, stay with you.

How to bring AI into your accounting and finance work

Bringing AI in finance and accounting into your team works best in small, proven steps.

You do not need to change everything at once, and you should not try to. The teams that adopt AI in finance and accounting successfully almost always start narrow, prove it works on their own real data, and only then widen the circle. Think of it less like installing software and more like training a new junior team member: you give them one well defined job, you check their work closely at first, and you hand over more responsibility only as trust is earned. The steps below are a sensible order for someone starting from zero.

- Pick one high volume, rule based process to begin with. Choose something you do many times a month that follows fairly predictable rules, such as reading purchase invoices, matching bank entries to the books, or sorting expense receipts into the right ledger heads. High volume means the time you save adds up quickly, and rule based means there is usually a clearly correct answer, which makes it far easier to tell whether the AI got it right.

- Choose a tool and a model that actually fit that job. Different tasks need different strengths, so match the tool to the work rather than picking whatever is most talked about. A simple, well structured task like reading a clean digital invoice may only need a small, fast and inexpensive model, while messy scanned documents or judgement heavy coding decisions may justify a more capable and more costly one. Confirm the tool handles your document formats and your language mix, and check where your data is processed and stored before you commit. Most AI tools are priced by usage, so your running cost rises with the volume you process, which is worth estimating up front.

- Run it alongside your current process for a few weeks. Do not switch anything off. Keep doing the work exactly as you do today, and run the AI on the same documents in parallel so you have two answers to compare. This shadow period, typically two to four weeks, costs you a little extra effort but tells you honestly how the tool behaves on your own workload rather than on a vendor demo.

- Check accuracy on your own real documents. Generic accuracy claims mean little until the tool has been tested on the invoices, statements and vouchers you handle every day, with your suppliers, your formats and your quirks. Sit down with a sample of those parallel results and count how often the AI was right, where it went wrong, and what kind of error it made. Pay close attention to the things that carry real consequences, such as amounts, tax treatment under the GST slabs of 0, 5, 18 and 40 plus any special rates or cess, and the ledger an entry is posted to.

- Keep a human approving everything before it posts. In the early stages the AI should prepare the work, not finalise it. A person reviews and clicks approve before anything is posted to the books or filed, so the tool drafts and a qualified human decides. This keeps you in control, gives you a clear audit trail of who approved what, and means a mistake is caught at review rather than discovered later in a reconciliation or an assessment.

- Expand only once you genuinely trust it. When the accuracy is consistently high on your own data and your reviewers are routinely approving the AI output with few corrections, you can widen its role. Add the next process, raise the volume it handles, or let clearly low risk and high confidence items flow through with lighter checking while you keep tighter review on the trickier ones. Grow in deliberate steps, and let each step earn the next.

How to get better with AI over time

Getting better at AI in finance and accounting is a steady habit, not a one time setup.

Bringing AI in is the start, not the finish. The real gains in accounting and finance come from steadily improving how you use it, in much the same way a team gets better at any process through practice, shared learning and honest measurement. None of this requires a technical background. It mostly requires good habits and a little discipline, and the guidance below describes the habits that matter most.

- Write clearer instructions. The quality of what AI gives back depends heavily on how clearly you ask. Be specific about what you want, the format you want it in, and the rules it must follow, for example which ledger heads to use, how to treat rounding, or what to do when a field is missing. Tell it what to do when it is unsure rather than letting it guess, such as flagging the item for a human instead of forcing an answer.

- Save the instructions that work as reusable templates. When a particular way of asking reliably produces good results, do not retype it from memory each time. Keep a shared library of these proven instructions, labelled by the task they handle, so the whole team uses the same wording. This gives you consistent output across people and makes it easy to improve one central version rather than many private variations.

- Document your assumptions. Write down the rules and choices behind your setup, such as how a certain expense type is classified, which tax rate applies to a category, or how an ambiguous case should be handled. Clear documentation means a new team member can pick up the process, your reviewers know what the AI was told to do, and you have a record to point to if a result is ever questioned in an audit or a review.

- Train the team and share what works. AI is most useful when the whole team is comfortable with it, not just one enthusiast. Run short, practical sessions on the tasks people actually do, encourage them to share the instructions and tricks that worked well, and make it safe to surface the cases where the AI got it wrong. Those shared lessons are often where the biggest improvements come from.

- Measure time saved and error rates. Decide on a few simple numbers and track them over time, such as how long a task now takes compared with before, how often the AI output needs correcting, and where mistakes tend to cluster. Real numbers tell you whether the tool is genuinely helping, show you which processes are ready to expand, and give you an honest basis for deciding what to adopt next.

- Review outputs regularly so quality stays high. Quality can drift as your suppliers change, your document formats change, or the rules change, so do not assume that good results today mean good results forever. Set a regular rhythm, for example a monthly look at a sample of the AI output, to confirm accuracy is holding up, catch new kinds of error early, and update your instructions and assumptions whenever something shifts. Steady, attentive review is what keeps AI in finance and accounting reliable for the long run.

How AI in finance and accounting actually works

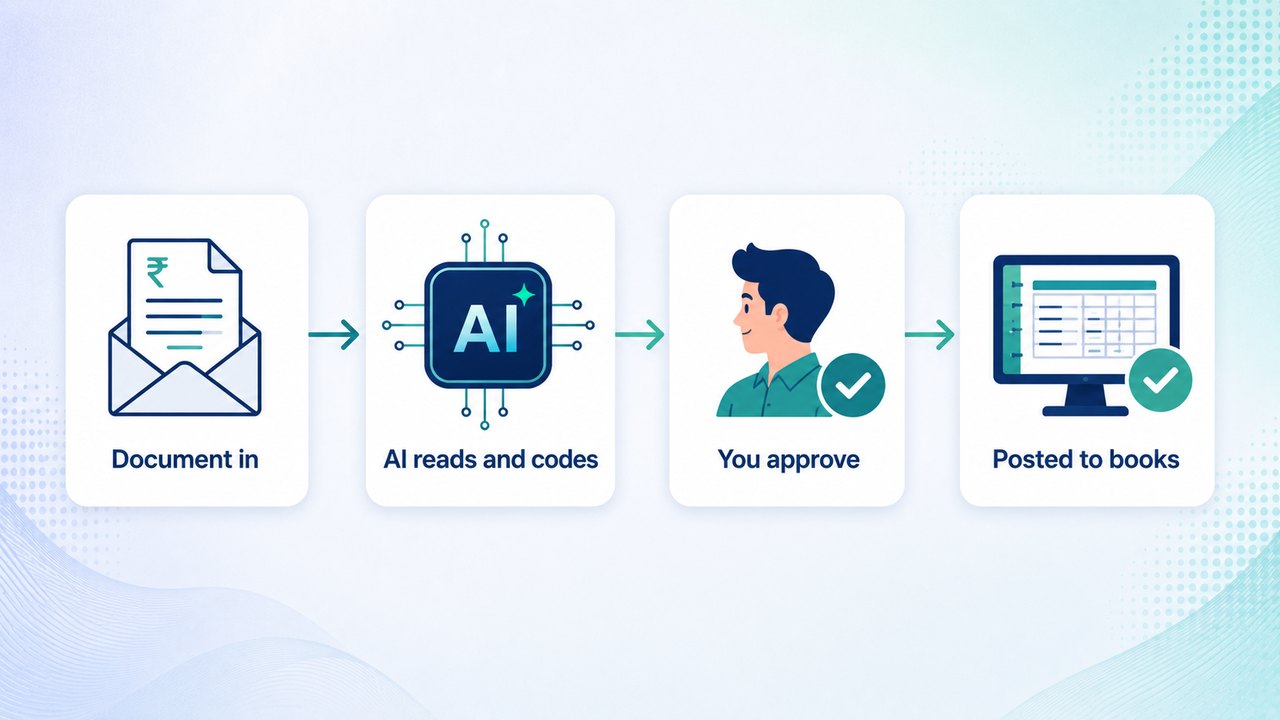

When people imagine AI in finance and accounting, they often picture a machine that takes over the books and quietly does the job on its own. That is not how it works in practice, and it is not how it should work. The honest picture is far less dramatic and far more useful. AI is a very capable assistant that reads, suggests and explains, while a qualified person stays in charge of every decision that actually counts. Once you understand the pattern, you can recognise it in almost every well built tool, no matter what it is called or who makes it.

The pattern follows a few clear stages, and the same stages repeat whether you are dealing with a purchase bill, a bank statement, an expense claim or a customer invoice.

Step one: something comes in

The process always begins with a piece of information arriving. This might be a supplier invoice as a PDF, a scanned receipt photographed on a phone, a bank statement, a spreadsheet of transactions or an email with an attachment. In the old way of working, a person would open each one, read it line by line and type the details into the accounting system by hand. That manual reading and typing is the slow, repetitive part, and it is exactly the part where AI can help first.

Step two: the AI reads it and proposes a treatment

The AI then reads the document the way a trained junior would, except much faster. It picks out the things that matter, for example the supplier name, the invoice number, the date, the taxable value, the tax charged and the total. For a tax line it can recognise whether a rate looks like one of the current GST 2.0 slabs of 0, 5, 18 or 40, and it can flag when a special rate or a cess might apply instead.

Crucially, the AI does not just extract numbers. It also proposes a treatment. In plain terms, it suggests what should happen to this document in the books. It might say that this looks like a purchase of office supplies, that it should go to a particular expense ledger, that the tax appears to be input tax that can be claimed, and that the amount should be recorded against a particular supplier. Think of this as a draft entry, complete with the AI’s best guess and, in good tools, a short note on why it reached that conclusion. Some tools also show a confidence level, which is an estimate of how sure it is and is not always reliable. A clean, typed invoice from a familiar supplier might come back with high confidence. A blurry photo of a handwritten bill in an unusual format might come back with low confidence and a polite request for a human to look closely.

Step three: a person reviews and decides

This is the most important stage, and it is the one that must never be removed. The AI has proposed. Now a person reviews. A qualified reviewer looks at the suggested entry next to the original document, checks that the figures match, confirms that the chosen ledger and tax treatment are correct, and either approves it, edits it or rejects it. The AI proposes and a human decides. That single sentence is the heart of how AI in finance and accounting should operate. The machine does the heavy lifting of reading and drafting, but professional judgement, accountability and the final call stay with a person who understands the business and the rules.

This division of labour is what makes the technology genuinely helpful rather than risky. The reviewer is no longer typing from scratch. They are checking and confirming, which is faster and less error prone, while still applying real expertise to anything unusual, ambiguous or material.

Step four: the entry is recorded

Once a person approves the proposed treatment, the entry is recorded in the accounting system in the normal way, as a clean, posted transaction. From this point onward it behaves exactly like any entry a person made by hand. It can be reported on, reconciled, included in returns and audited. Nothing about it is mysterious or special. The only difference is that a draft was prepared for review rather than typed line by line, which saved time at the start.

Step five: every step is logged so it can be traced

A well designed tool keeps a record of the whole journey. It logs what came in, what the AI proposed, who reviewed it, what they changed, when they approved it and what was finally recorded. This is the audit trail, and it matters enormously in accounting and finance. If a question comes up months later, you can trace any number back to its source document and see exactly how it was handled and by whom. This traceability is not an optional extra. It is what lets you trust the process, satisfy an auditor and correct anything that later turns out to be wrong.

So the full loop is simple to remember. Information comes in. The AI reads it and proposes a treatment. A person reviews and decides. The approved entry is recorded. Every step is logged so it can be traced. If you keep that shape in mind, you will be able to evaluate almost any AI feature on its merits and ask the right questions before you rely on it.

Using AI responsibly in accounting and finance

Responsible AI in finance and accounting comes down to a few firm habits.

AI can save real time and reduce drudgery, but it has to be used with care, especially when you are handling other people’s money and confidential records. Responsible use is not complicated, and it does not require a technical background. It comes down to a handful of habits that protect your clients, your firm and your professional standing. Treat the points below as a standing checklist for any tool you bring into your work.

Keep a person in the loop for approvals

This is the single most important habit for safe AI in finance and accounting.

The single most important safeguard is to keep a qualified person in the approval path. AI should propose, suggest and draft, but a human should approve anything that gets posted, filed or sent. Do not set up a fully automatic flow that records entries or submits returns with no one checking the result, however tempting that might be on a busy day. Human review is what keeps accountability where it belongs, with the professional, and it is your last line of defence against a confident but wrong suggestion. The more material the item, the more careful the review should be.

Protect sensitive data and never paste confidential client data into tools you do not control

Financial records are sensitive. They contain client names, bank details, salaries, contracts and figures that must stay private. A simple, firm rule will keep you safe: do not paste confidential client data into tools you do not control. That includes free public chat tools and any service where you cannot be sure what happens to the information after you submit it. If you want to test how a tool behaves, use dummy data or a generic example with no real names and no real numbers. Before you put any genuine client information into a system, you should know who can see it, where it is stored and what the provider is allowed to do with it. Data protection and privacy laws set rules for handling personal data, so make sure any tool you use fits those obligations.

Prefer tools that do not train third party models on your data

When you do choose a tool for real work, prefer one that does not use your data to train third party models. In plain terms, your clients’ information should be used to do the job you asked for and nothing else. It should not quietly become training material that could surface elsewhere. Reputable providers state this clearly in their terms and their privacy documentation, and they offer business arrangements that keep your data yours. If a provider is vague about this, treat that as a warning sign and look elsewhere.

Always keep an audit trail

A clear trail is what makes AI in finance and accounting defensible later.

Insist on tools that keep a complete, time-stamped record of what was proposed, who approved it and what was finally recorded. An audit trail protects you in three ways. It lets you trace any number back to its source, it lets you show an auditor or a regulator exactly how a figure was arrived at, and it lets you find and fix mistakes quickly if something was handled wrongly. If a tool cannot tell you who did what and when, it is not ready for serious accounting and finance work.

Watch for bias and check the reasoning

AI learns from data and can carry bias into its outputs, for example by always coding a certain vendor the same way or favouring a pattern that is not actually correct. Do not only check the final number, check the reasoning behind it where the tool shows it, and stay alert to any output that looks skewed or that quietly disadvantages one customer, vendor or category. Fairness is one of the principles regulators expect, so treat it as part of your review.

Treat every output as a draft to be checked

This one mindset keeps AI in finance and accounting reliable.

Finally, build one mindset into everything you do with AI: every output is a draft until a person has checked it. The technology is impressive and often right, but it can hallucinate, which means inventing a plausible looking number, field or explanation that is simply not there, it can be confidently wrong, it can misread an unusual document, and it does not understand the context of your client or the latest change in the rules the way you do. So read what it gives you, compare it against the source, and apply your own judgement before you rely on it. Used this way, AI becomes a fast, tireless assistant that frees you for the work only a professional can do, rather than a black box you have to take on trust.

These habits are not unique to any one firm or product. They reflect a wider direction of travel for the whole sector. A major financial regulator published its framework for responsible and ethical AI for the financial sector, and the principles in it, accountability, fairness, transparency and keeping humans responsible for outcomes, line up neatly with the simple safeguards above. If you adopt AI in finance and accounting with these habits in place, you get the benefits of speed and scale while keeping the trust, accuracy and accountability that your profession depends on.

Where ReconScribe fits in

Everything above works with general AI tools, and you can start with nothing more than the steps in this guide. If you would rather have this built into your accounting workflow so it runs every day without copy and paste, that is what we build at ReconScribe. In short, the app:

- Reads your invoices and posts them to your accounting system after you approve, with the right GST and ledgers

- Reconciles GST against your GSTR-2B and flags the gaps

- Gives you an MIS dashboard, live today

- Adds AI bank reconciliation, coming soon

To go further, read our hands on guide to AI prompts for finance, see accounts payable automation in practice, try the GST calculator or browse our free finance calculators. Questions? Write to contact@reconscribe.com.

To go deeper on a specific tool, see our hands-on guides to Claude for finance and accounting and OpenAI Codex for finance.

AI in finance and accounting FAQ

Common questions about using AI in finance and accounting, answered plainly.

What can AI actually do for finance and accounting work today?

AI in finance and accounting is good at reading documents, drafting text, summarising long files, classifying transactions, suggesting ledger codes, and answering plain language questions about your data. It can extract fields from an invoice, draft a polite payment reminder, explain a tax concept, or propose how to categorise a bank line. Think of it as a fast, tireless junior assistant that prepares work for you to review, not a qualified person who signs off on its own.

Is AI accurate enough to trust with financial numbers?

AI is often very good at language and pattern tasks but it is not a calculator and it does not guarantee correct arithmetic or correct figures. It can read an invoice total correctly most of the time, yet still misread a smudged digit, swap two numbers, or confidently state a wrong tax rate. Treat every number it produces as a draft that a human checks against the source document, especially for filings, payments, and anything that leaves your office.

Where is AI weak or genuinely bad at finance work?

AI is weakest at exact arithmetic across many rows, at applying the precise current rule when laws have just changed, and at anything needing real judgement about intent or materiality. It struggles with messy multi step reconciliations, with deciding whether an expense is allowable, and with edge cases that are rare in its training. It also has no real sense of your business context, so it cannot know that a particular large payment is normal for you while another is suspicious.

What should I always double check in AI output?

Always check the numbers, the dates, the tax rates and the totals against the original document, because these are exactly where small errors do the most damage. Verify any legal or rule based claim against an official source, since rules change and the AI may be out of date. Also confirm names, GSTINs, PAN, account numbers and bank details character by character, as a single wrong digit can send money to the wrong place.

Can AI make up numbers or facts (what is hallucination)?

Yes, AI can hallucinate, which means it can produce a confident answer that is simply invented, including fake figures, fake rule citations, or a total that does not match the invoice. This happens because the AI is predicting plausible text, not retrieving verified facts, so a wrong answer can look just as polished as a right one. The practical defence is to never accept a number or a citation without tracing it back to the source, and to be most careful when the AI sounds most certain.

Will AI replace accountants?

No, AI is far more likely to change the work than to remove the people, by taking over repetitive data entry and first draft tasks while leaving judgement, client relationships, advice and sign off to humans. The accountants who do best will be the ones who learn to direct AI well and to catch its mistakes, rather than those who ignore it. Responsibility for a filing or a set of accounts still sits with a qualified person, and a tool cannot carry that responsibility for you.

Which AI model is best for finance and accounting?

There is no single best model, because the leading ones change every few months and each has strengths, so the better question is which tool fits your task, your budget and your data rules. For most finance teams the practical choice is a well known general assistant for drafting and questions, plus a more specialised or document focused tool for extracting data from invoices and statements. Try two or three on your own real examples for a week and judge them on accuracy and how easily you can check the output, not on marketing claims.

How do I start using AI in finance and accounting?

Start small with one low risk, high volume task such as drafting emails, summarising a long document, or extracting fields from a batch of invoices, and run it alongside your normal process so you can compare. Keep a human reviewing everything at first and note where the AI helps and where it slips. Once you trust it on that one task, expand carefully to the next, rather than trying to automate the whole month end at once.

Is it safe to put financial data into AI, and what about the DPDP Act?

It depends entirely on the tool and its settings, so before pasting client or company data you must know where it is stored, whether it is used to train the model, and who can see it. Prefer business or enterprise plans that contractually do not train on your inputs, and avoid free consumer tools for sensitive data. Your local data protection law treats personal data seriously, so you should minimise what you share, mask or remove personal identifiers where you can, and check that your provider’s terms support your obligations as the party responsible for that data.

Do I need to be technical to use AI?

No, you do not need to code or understand the technology to use AI well, because most tools work through plain typed instructions in everyday language. What matters far more is your domain knowledge, since a good accountant who knows what a correct answer looks like will get far better results and catch errors a non expert would miss. The main skills to build are writing clear instructions and reviewing output critically, both of which you can learn in a few weeks of practice.

Can AI post accounting entries automatically?

Technically yes, AI can suggest entries and software can be set up to post them, but fully automatic posting with no human review is risky for anything that affects your books or filings. A safer pattern is to let the AI prepare the entry, show its suggested accounts and amounts, and require a person to approve before it posts. Reserve any straight through automation for very predictable, low value, high volume items, and keep a clear audit trail and the ability to reverse mistakes quickly.

Can AI do GST and reconciliation work?

AI can help a lot with the preparation steps, such as reading invoices, matching purchase records to the supplier data, flagging mismatches, and drafting explanations, which saves real time on reconciliation. It is less reliable on the final rule application, so any GST rate it suggests should be checked against the current slabs, which under GST 2.0 are 0, 5, 18 and 40 percent with special rates and cess possible on certain goods. Use AI to narrow down and explain the exceptions, then have a person confirm the treatment and the final figures before you file.

How much does AI cost?

Costs range widely, from free consumer tiers that are unsuitable for sensitive data, to paid individual plans of a few hundred to a couple of thousand rupees per user per month, up to specialised document or workflow tools priced per page or per transaction. The honest way to budget is to estimate the time saved on a real task and compare that against the subscription, rather than chasing the cheapest option. Remember to add the cost of training your team and of the review time that AI never removes, since a careless rollout can cost more than it saves.

How do I write a good prompt?

A good prompt gives the AI a role, the context, the exact task, and the format you want back, for example asking it to act as an accounts assistant, summarise the attached statement, and return the result as a table of date, description and amount. Be specific about constraints such as the period, the currency, and that it must not guess missing values but flag them instead. If the first answer is off, refine your instruction rather than starting over, and keep a small library of prompts that worked well for tasks you repeat.

Can AI read scanned or handwritten documents?

Yes, modern AI can read scanned PDFs, photos of invoices, and even some handwriting, which is genuinely useful for the piles of paper that finance teams deal with. Accuracy drops with poor scans, faint print, stamps over text, regional handwriting and unusual layouts, so a clean, well lit, straight image gives much better results than a crumpled photocopy. Because misreads do happen, always verify the captured numbers and key fields against the original before you rely on them, particularly amounts and tax identifiers.

How do I get my team to adopt AI in finance and accounting?

Adoption works best when you pick one painful, repetitive task, show a small win on real work, and let the team see time saved rather than announcing a grand transformation. Be honest about the limits and the need to check output, so people trust the tool instead of either fearing it or over relying on it. Give a little training, name a curious team member as the go to person, and write down simple rules about what data can go in and what must always be reviewed, so good habits spread on their own.

If you want the underlying spreadsheet skills, our Excel formulas for finance guide covers the 15 most useful ones.

If you have not settled on a core accounting system yet, our accounting software comparison by country is a good starting point.